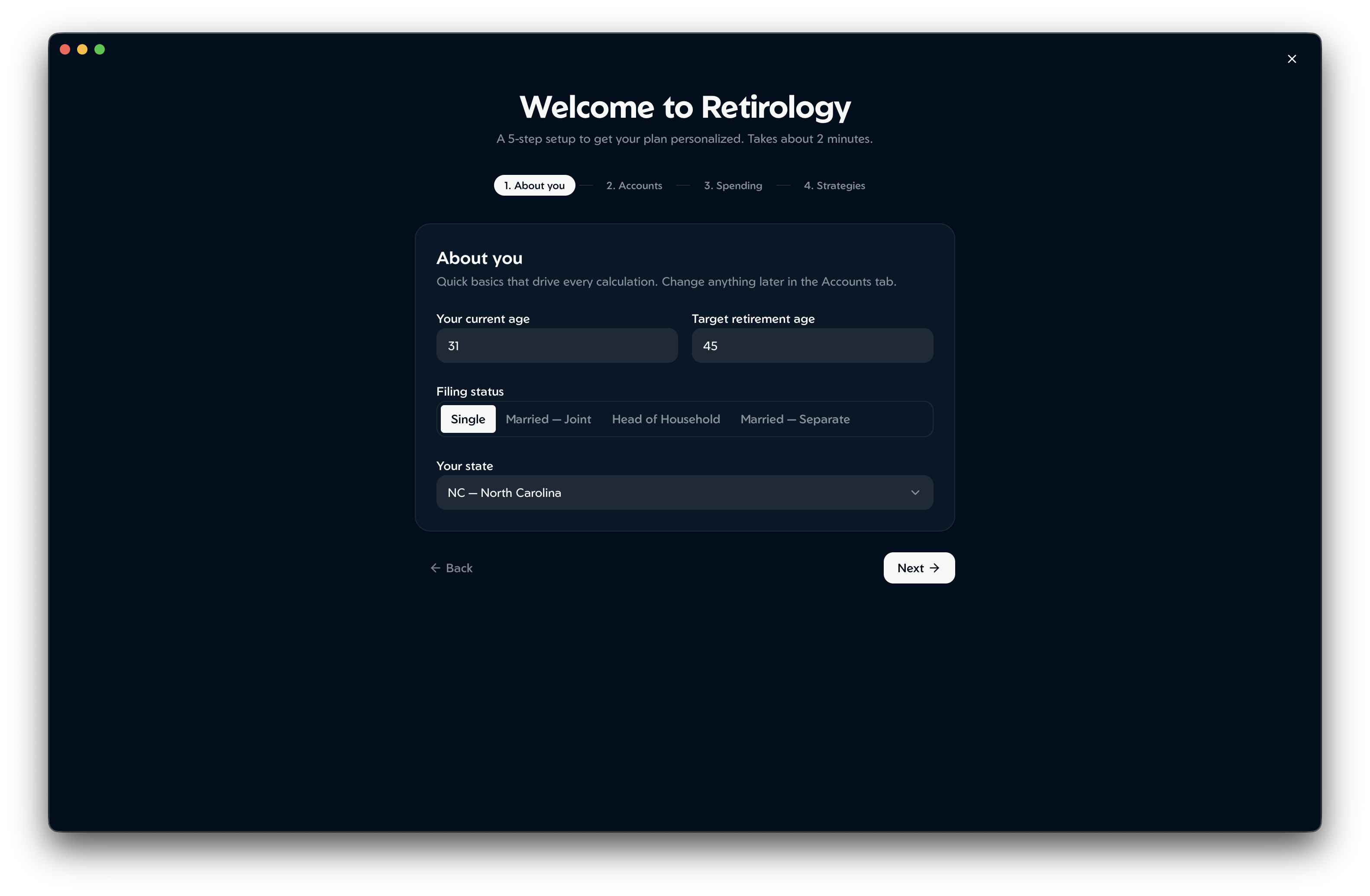

Two-minute onboarding

A four-step wizard — about you, accounts, spending, strategies — gets a plan personalized in roughly two minutes. Defaults are sane, every value is editable later, and nothing locks you in.

Buy once · Every future version free

Professional-grade retirement analysis as a one-time purchase — not a $20–$40/month rental. Roth conversion ladders, Monte Carlo, ACA optimization, full 51-state tax modeling. Runs on your machine. No accounts. Your numbers stay yours.

macOS · Windows · Linux

$19+ once, never again · No subscription · No accounts · No data collection · Runs offline

What it does

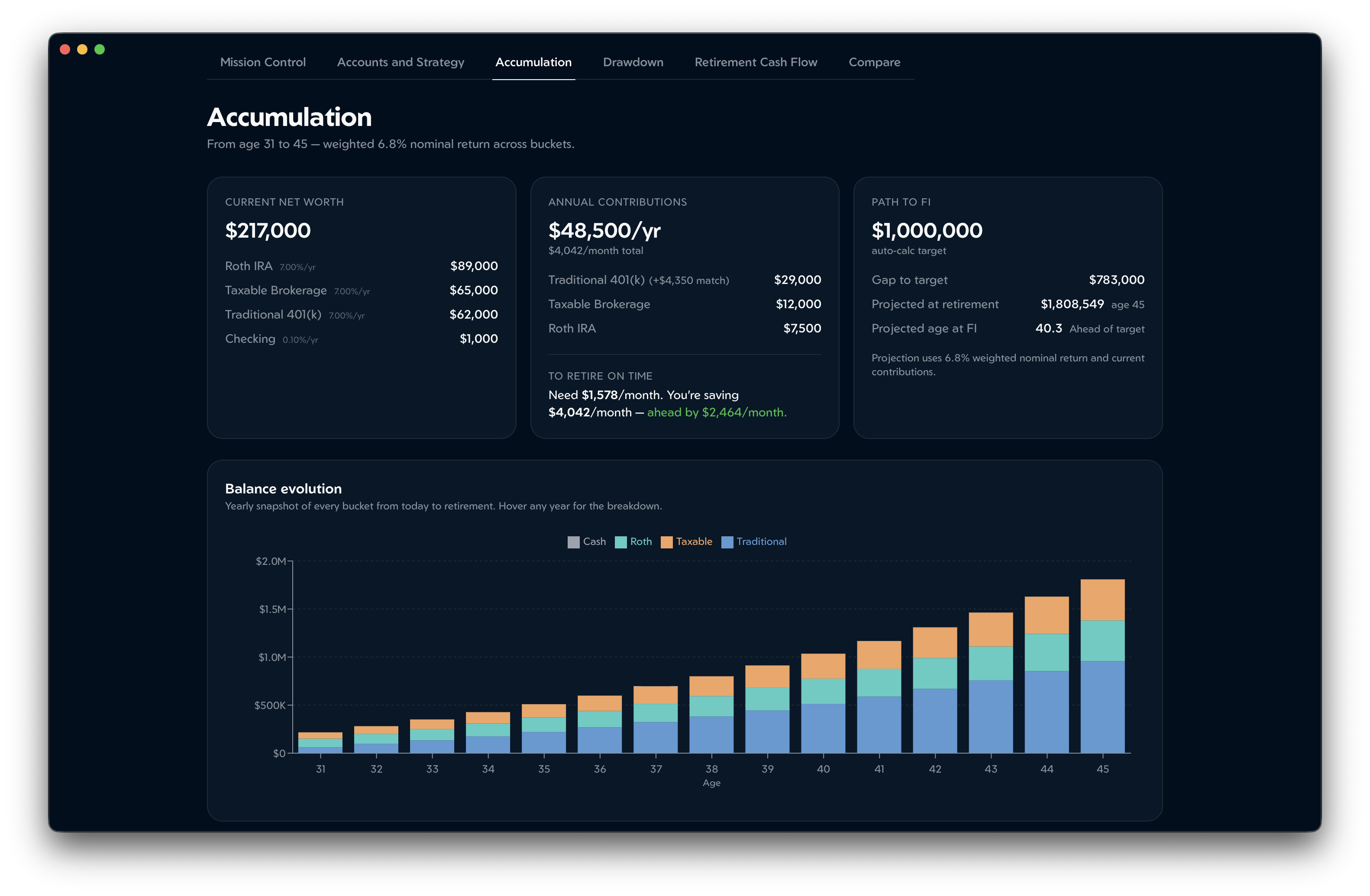

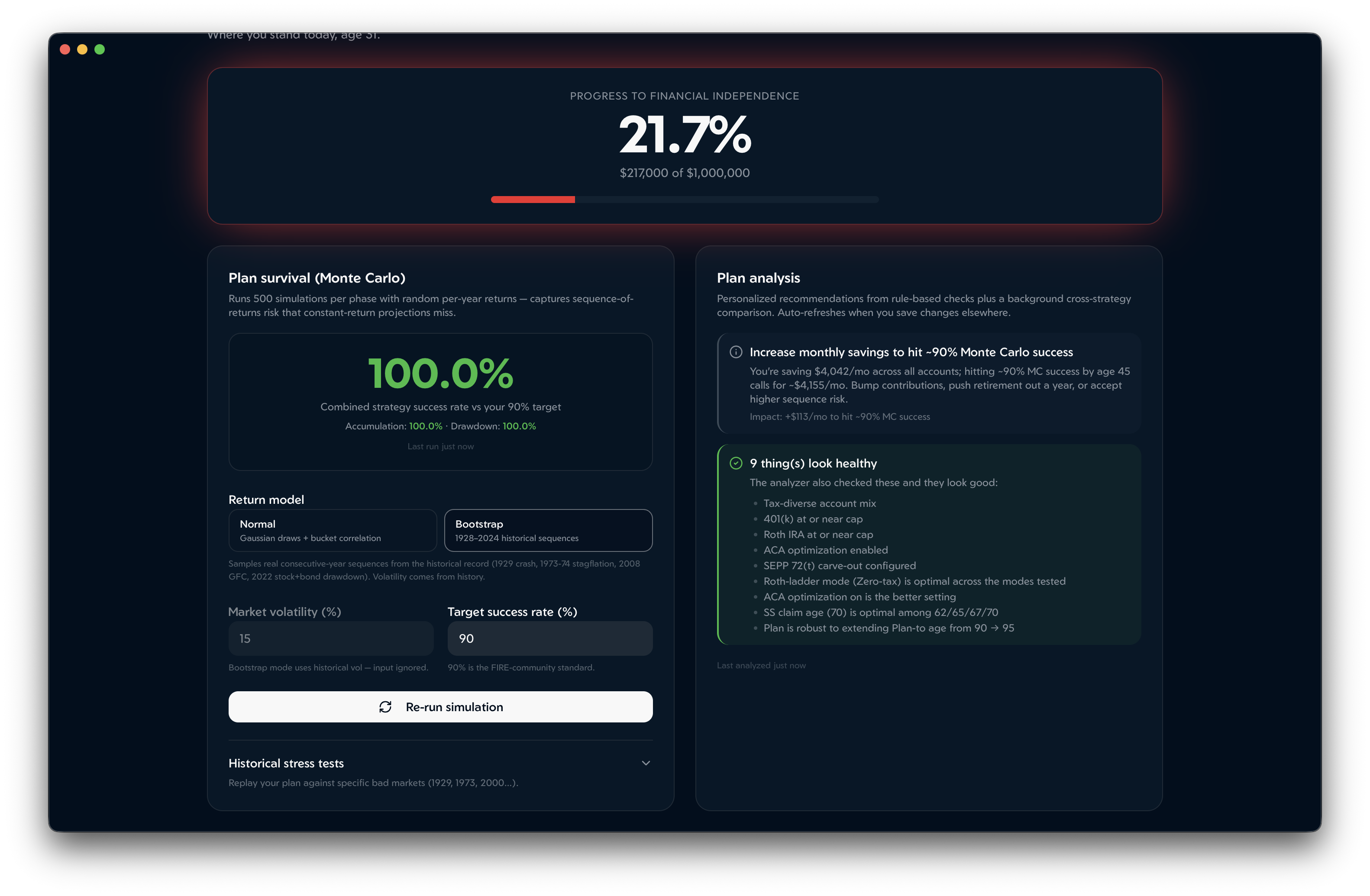

Most retirement calculators give you a single number. Retirology models the whole arc — accumulation through drawdown — and lets you stress-test the plan against bad markets, tax law, and your own assumptions.

A four-step wizard — about you, accounts, spending, strategies — gets a plan personalized in roughly two minutes. Defaults are sane, every value is editable later, and nothing locks you in.

Multi-bucket accumulation modeling — taxable, traditional, Roth, HSA — with per-account growth rates, employer match, HSA tax credit, and inflation-adjusted projections. Your FI target is derived from a built-in budget analyzer (category-by-category), so it reflects what you actually spend, not a guessed round number.

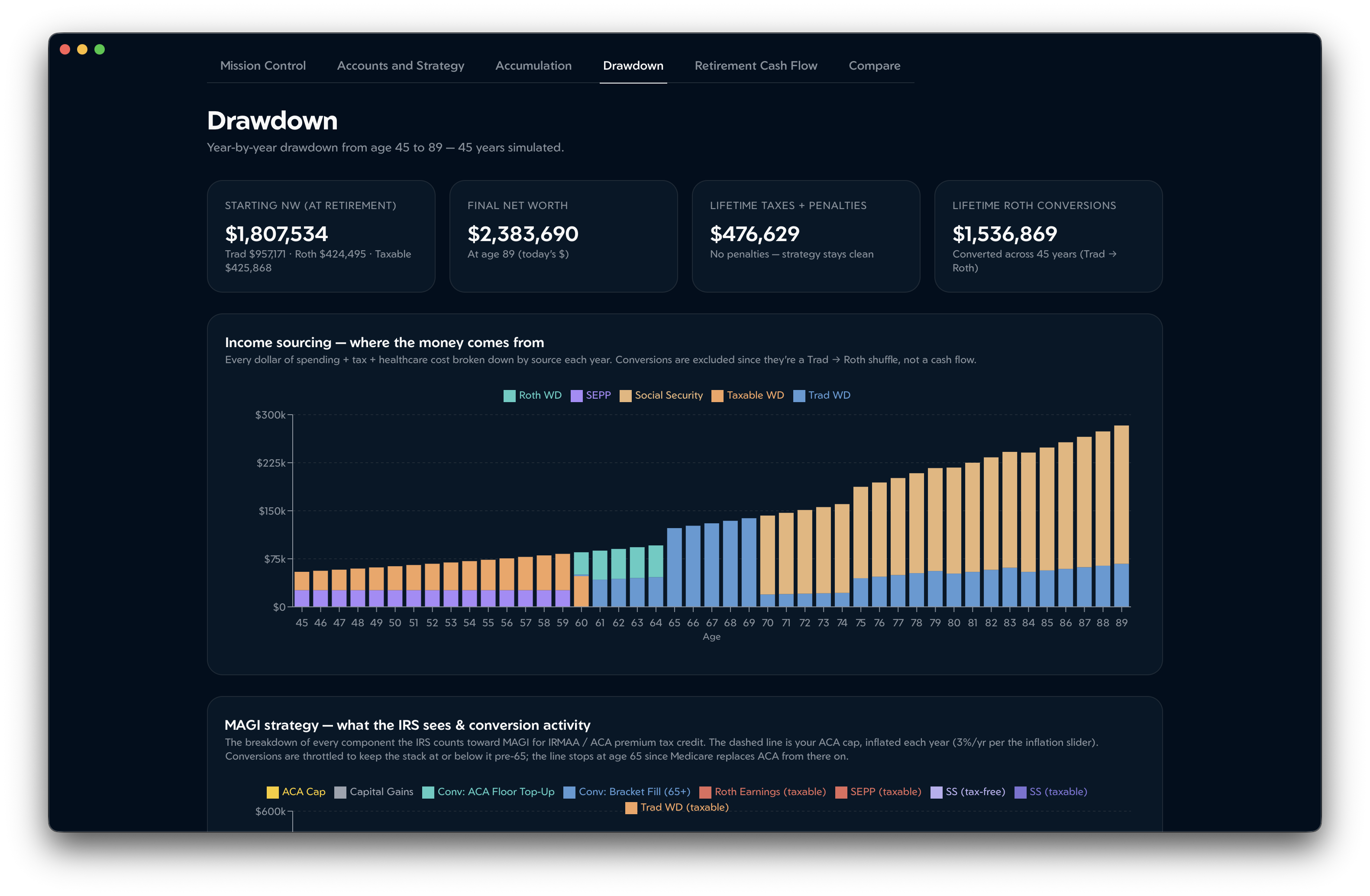

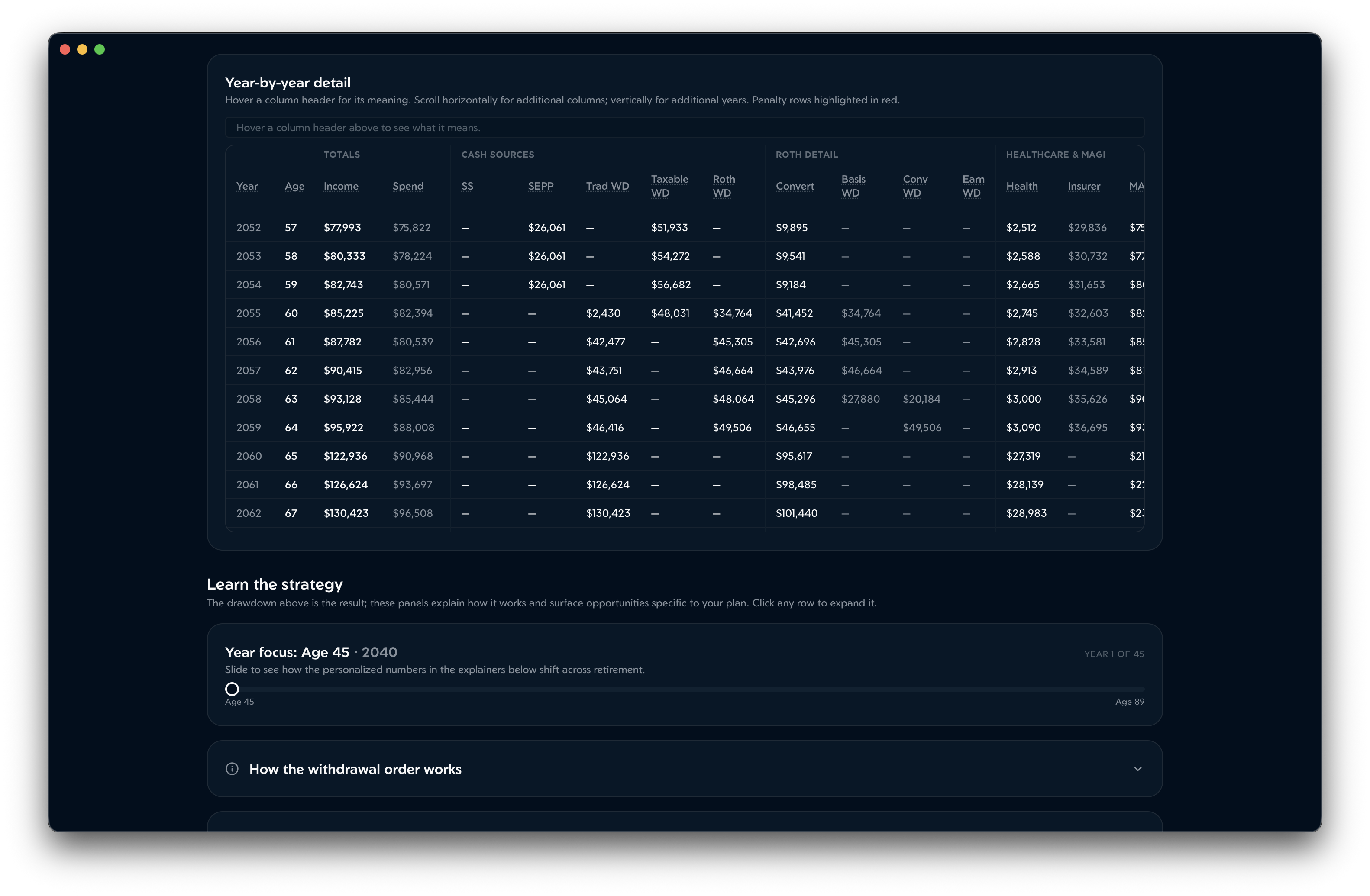

Year-by-year retirement simulation with income sourcing, MAGI strategy, ACA premium-subsidy optimization, SEPP 72(t), RMDs, Social Security claim ages, and full state + locality income tax for 51 states — across all four federal filing statuses (single, MFJ, head of household, MFS).

Four ladder modes — fill-the-bracket, ACA-cap, fixed-amount, and target-RMD — with year-by-year schedules showing conversion amounts, taxes paid, and the resulting Roth balance through your modeled retirement horizon.

Normal-distribution sampling and historical bootstrap mode pulling from a bundled 1928–2024 dataset (S&P 500, 10-yr Treasury, T-bills, CPI). Get a real success-rate distribution, not a single optimistic line.

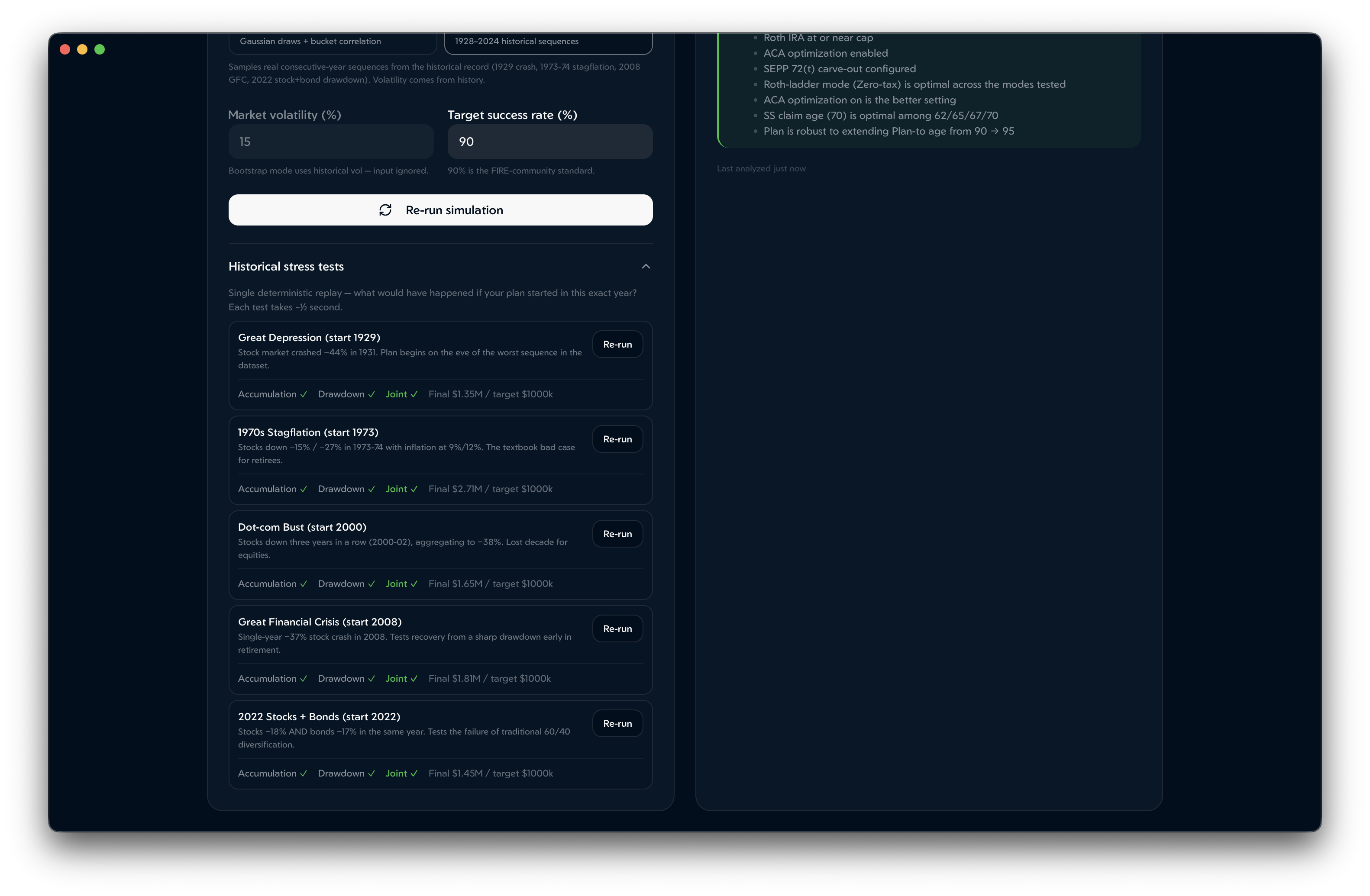

Replay your plan against the actual sequences from 1929, 1973–74, 2000, 2008, and 2022. See exactly when a real bad market would have broken it — and by how much.

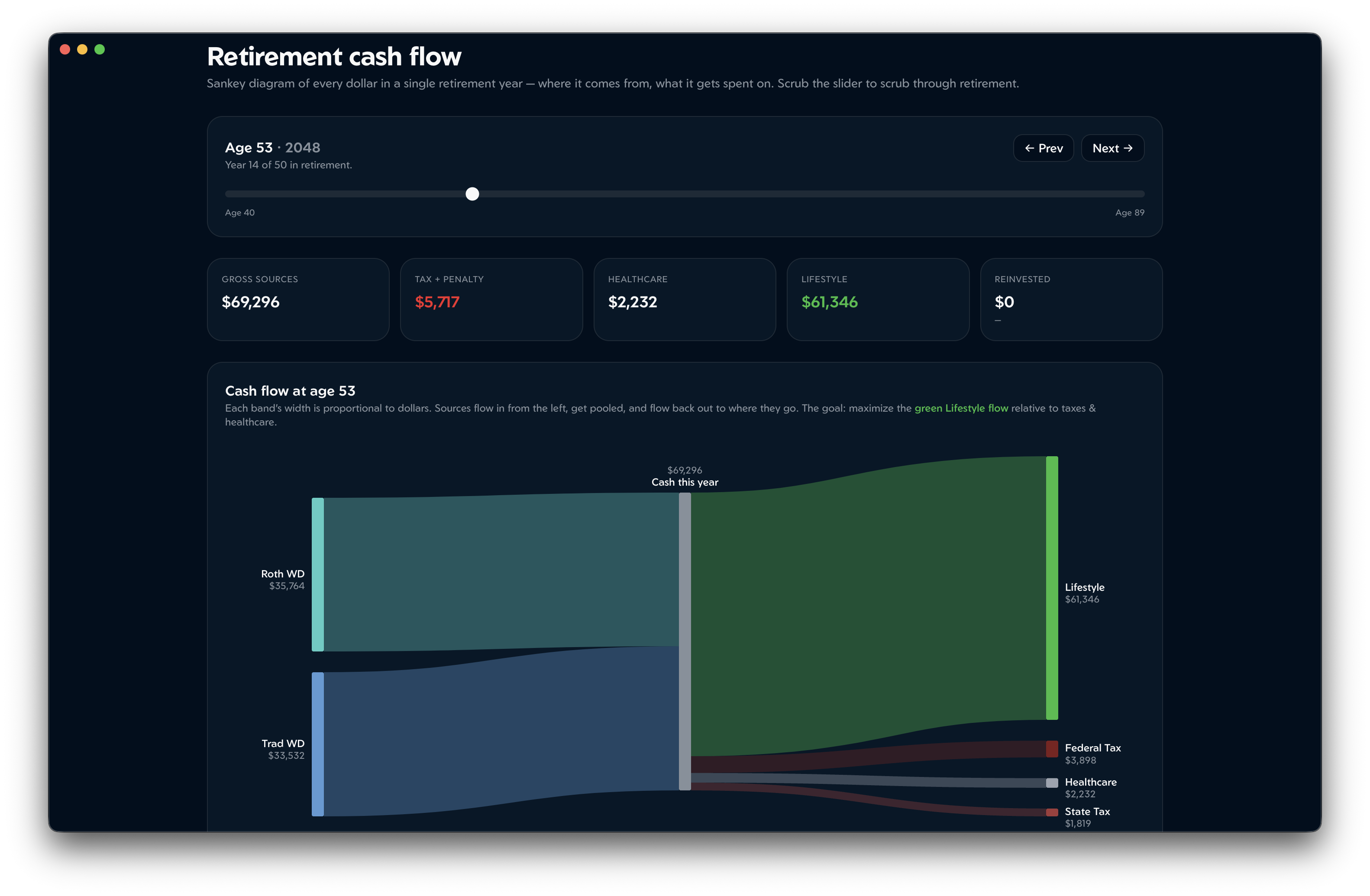

Trace every dollar through retirement — from accounts and Social Security through Roth conversions, taxes, ACA premiums, and spending. See where the money actually goes.

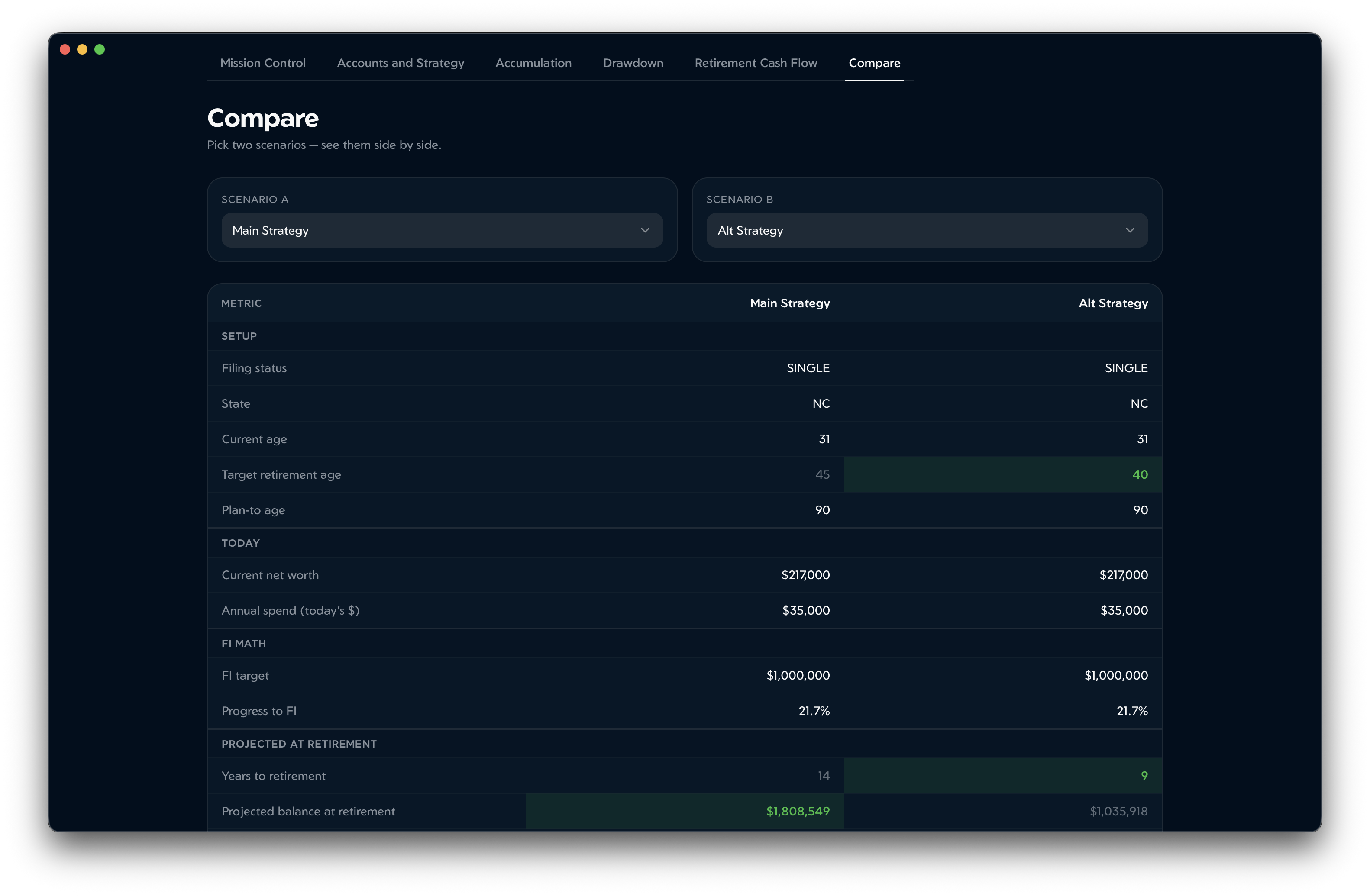

Save plans, then put any two side by side — different claim ages, ladder strategies, retirement years, geographies. The optimizer surfaces the meaningful differences automatically.

Alternative to

If you've been comparing budgeting tools like YNAB or Monarch, paid retirement planners like ProjectionLab, Boldin (formerly NewRetirement), MaxiFi Planner, or Pralana, or you've outgrown the Personal Financial Toolbox spreadsheets — Retirology covers what most of them do (and more), at a one-time price typically less than a single year of any of their subscriptions.

Typical subscription planner

$240–$480 / year, every year

$20–$40/month — paid in perpetuity

Retirology

One-time$19+ once

$65 suggested — about a single month of an advisor

Even at the suggested $65 tier, Retirology costs less than two months of a typical subscription planner — and you keep using it after.

Privacy isn't a tagline

Most retirement tools want you to upload your entire net worth to their servers. Retirology runs the math locally. We have nothing to leak because we have nothing to collect.

Verify it yourself. Run any network monitor (Little Snitch on Mac, your firewall, Wireshark) and confirm: exactly one HTTPS GET to retirology.app/version.json per launch. Nothing else.

A once-per-launch fetch of retirology.app/version.json to check for updates. It's a static file. No headers about you, no IDs, no telemetry.

Every account, every scenario, every dollar lives in one file on your disk. Back it up, encrypt it, delete it. Your call.

There's nothing to sign up for. The app launches and works. The only thing you give us at purchase is an email — for the receipt.

No Google Analytics, no Mixpanel, no Sentry, no chat widget. Not in the app. Not on this website.

Honest pricing

Retirology is a one-time purchase with a $19 floor — pick the tier that feels fair. Buy once and every future version is yours free. There's just one product; the tier you choose is what you pay.

Floor

$19 one-time

The minimum. Same app, same features. Pay what you can — no judgment.

Suggested

Most pick this$65 one-time

Roughly a single month of a typical advisor subscription — except you own it, updates and all.

Generous

$200 one-time

For folks who want to back the project meaningfully. You can also enter a custom amount in checkout.

Every update is free, forever — patches, new features, and the annual releases with refreshed tax tables. Buy once, and you never pay again. Re-download any version anytime from your account.

Affiliate program

Because Retirology's price is set by the customer above a $19 floor, there's no per-sale ceiling on what you earn. Most affiliate programs cap your commission at a percentage of a fixed price. Ours scales with whatever the buyer actually pays.

If they pay $19

$3.80

your commission

If they pay $65

$13.00

your commission

If they pay $200

$40.00

your commission

Questions

Nothing in the software. The app and every feature are identical regardless of tier. The price you choose is what funds the next release. $19 is the floor; $65 is what we suggest if it's not a stretch; $200 is for folks who want to back the project.

No. You pay once and own it. Every update after that — bug-fix patches, new features, and the annual releases with refreshed tax tables — is free, forever. There's no renewal, no per-year charge, nothing to cancel.

Stays on your machine in a single SQLite file. We don't see it, can't read it, and have no way to. See the privacy section or the full privacy statement for the per-OS file paths.

Never. Each year's release refreshes the tax tables and adds new features, and it's free for everyone who's bought Retirology — no upgrade fee, no discount code to hunt for. When a new version is out, the app points you to your account, where you re-download the latest build at no charge.

The app keeps working. There are no servers it depends on — the only network call is the once-per-launch update check, and if that fails the app just continues. Your data lives in a local SQLite file you own, so nothing remote is required for the app to function — and your last paid copy keeps running indefinitely.

macOS: the app is signed and Apple-notarized — you'll see the standard one-time "downloaded from the Internet, are you sure?" prompt the first time you open it. Click Open and you're in. Windows: SmartScreen flags installers without an established reputation — click More info → Run anyway. (An EV signing cert is on the post-launch roadmap.) Linux: chmod +x the AppImage and run it.

A modest one-time price keeps the project sustainable without ads, accounts, subscriptions, or upsells — which is the whole point. The $19 floor is intentionally low; if it's genuinely out of reach, email contact@retirology.app and we'll work something out.

Download once, plan forever. macOS, Windows, Linux. No account needed.